If you’ve ever wondered why some people build wealth effortlessly while others struggle despite saving regularly—compound interest is usually the answer. It’s not magic; it’s math. Once you understand it and use a compound interest calculator to visualize your future growth, you’ll never think about money the same way.

The short answer: Compound interest is interest calculated on both your original principal and the interest you’ve already earned. Unlike simple interest, it grows on itself – which means your money accelerates over time, not just grows.

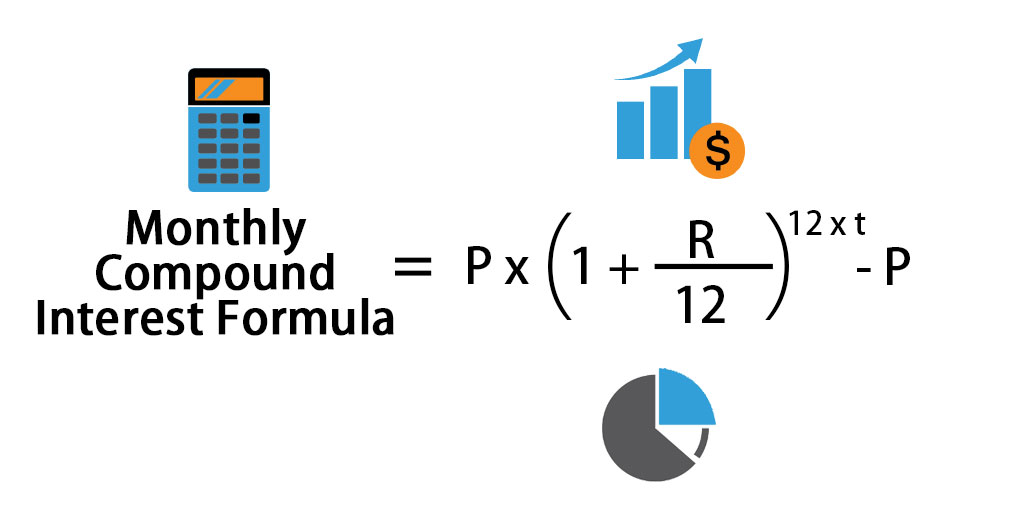

The Formula (Without the Headache)

The compound interest formula: A = P (1 + r/n)^(nt)

| Variable | What It Means |

|---|---|

| A | Final amount (what you end up with) |

| P | Principal (your starting amount) |

| r | Annual interest rate (in decimal form) |

| n | Number of times interest compounds per year |

| t | Time in years |

So if you invest $10,000 at 8% annual interest, compounded monthly, for 20 years – you end up with $49,268. That’s nearly 5x your money without adding a single extra dollar.

Simple Interest vs. Compound Interest: The Real Difference

| Starting Amount | Rate | Years | Simple Interest | Compound (Monthly) |

|---|---|---|---|---|

| $10,000 | 8% | 5 yrs | $14,000 | $14,898 |

| $10,000 | 8% | 10 yrs | $18,000 | $22,196 |

| $10,000 | 8% | 20 yrs | $26,000 | $49,268 |

| $10,000 | 8% | 30 yrs | $34,000 | $109,357 |

Notice what happens at 30 years – compound interest produces over 3x more than simple interest on the same amount. Time is the multiplier.

How Compounding Frequency Affects Your Returns

The more often interest compounds, the more you earn. Here’s how frequency changes the outcome on $10,000 at 8% over 10 years:

| Compounding Frequency | Final Amount |

|---|---|

| Annually | $21,589 |

| Quarterly | $22,080 |

| Monthly | $22,196 |

| Daily | $22,253 |

A Real-World Example: Starting Early vs. Starting Late

Sarah invests $5,000/year from age 25 to 35 – then stops. Total invested: $50,000.

Mike waits until 35 and invests $5,000/year all the way to age 65. Total invested: $150,000.

Assuming 8% annual return – Sarah ends up with more money at 65. She invested one-third of what Mike did. The only difference? She started 10 years earlier. That’s the power of compounding.

How to Use a Compound Interest Calculator

Most online calculators ask for four things:

- Principal – How much you’re starting with

- Annual Interest Rate – The rate your investment or savings account offers

- Compounding Frequency – Monthly, quarterly, annually

- Time Period – How many years you plan to keep the money invested

Some calculators also allow monthly contributions, which is where things get really powerful. Even adding $100/month to a $5,000 starting amount at 7% over 25 years turns into over $85,000.

Key Factors That Determine Your Compound Growth

- Starting amount – More principal = bigger base to grow from

- Interest rate – Even 1-2% difference has massive long-term impact

- Time horizon – The single most powerful variable

- Compounding frequency – More frequent = slightly better returns

- Consistent contributions – Regular deposits supercharge growth

The Mistake Most People Make

Waiting. That’s it. People wait until they have ‘enough’ to start investing. But with compound interest, waiting even 5 years can cost you tens of thousands in lost growth. Starting with $500 today beats starting with $5,000 five years from now in many scenarios.

The other mistake is withdrawing early. Every time you pull money out, you reset the compounding clock on that amount. Let it sit.

Bottom Line

Compound interest rewards patience above everything else. The calculator is just a tool – what matters is putting your money to work as early as possible and leaving it alone long enough for the math to do its thing.

The best time to start was yesterday. The second best time is today.